Should You Buy Nebius?

Nebius ($NBIS): The AWS of AI

Overview

What the Company Does

Today, Nebius is building a vertically integrated AI cloud.

But I don’t like this description, because I believe it does not properly explain the insane potential I see in Nebius.

I prefer:

Nebius lets customers outsource as much technical complexity as they want.

For highly technical customers, such as hyperscalers like Meta and Microsoft or frontier labs like Anthropic and OpenAI, less abstraction can be better. They get more control, more customizability, and can potentially pay less because they manage more of the stack themselves.

For less technical customers, more abstraction is better because Nebius removes more complexity and captures more value.

Win-win.

For highly technical customers like hyperscalers, such as Meta and Microsoft, that can mean bare metal GPUs.

For the long-term majority of customers, especially enterprises, it will however mean managed training, inference, or tokens through Token Factory.

Each customer can pick how much they want Nebius to “take care of them.” ;)

GPUs as a service → tokens as a service → end-to-end agents → results as a service.

Eventually, when agents in the digital world and robots in the physical world are reliable, scalable, and can deliver high-quality work end to end, Nebius might sell what I think of as “results as a service.”

I know this sounds abstract, so let me give a simple example.

If you want AI to handle customer support on your website, you do not care how many tokens Nebius generates for you.

What you care about is how many support cases Nebius handles, how fast they are resolved, and how happy the customers are.

So paying for a metric that captures both the quantity and quality of handled support cases would make much more sense than paying per token.

A token does not equal value.

A successfully handled support case does.

The customer should not care about GPUs. The customer should not care about tokens. Eventually, the customer may not even care about agents.

The customer pays money and gets the solution to the work that needs to be done, without touching infrastructure, hardware, APIs, or any of the technical complexity underneath.

This is not just my long-term view on Nebius. It is my long-term worldview on AI investing in general.

In the short term, of course, GPUs and tokens remain highly relevant. That is where the revenue is today.

But the long-term direction is abstraction.

It is my personal view that the entire AI industry eventually has to move away from cost-based pricing to value-based pricing.

This will ultimately remove most objections to scaling AI and resolve most ROI conversations.

To me, this is obviously the way to go.

Why Now?

Because I believe we are still at the very beginning of actually useful agents that can solve tasks end to end.

Agents are only starting to become real. And I do not think people are ready for the incredible amount of work that can and should be done by them.

Agents will be like having a trillion 200 IQ workers operating 24/7, in parallel, with better coordination, less friction, and fewer emotional problems, needs, or drama than humans.

This is what completely breaks all financial models from economists, traditional investors, and finance bros.

How much do you think they would expect the US economy to grow if they seriously assumed trillions of geniuses were entering the US workforce?

That is what is happening with AI right now.

Current models do not reflect that!

To the contrary, they think we are in a giant bubble because they look at things like the Shiller PE, the Buffett Indicator, and other metrics that are horrible in this context because they do not reflect this unique, unprecedented technological supercycle at all.

If there is one thing you take away from this article, it should be this insight:

To properly account for the massive benefits of AI, your models must be incredibly aggressive.

The technological progress is truly mind-blowing.

Stanford’s 2025 AI Index showed that the cost of running a model at GPT-3.5-level performance dropped by more than 280x between November 2022 and October 2024. Depending on the task, inference prices have been falling by 9x to 900x per year.

The cost of intelligence, the most valuable resource in the universe, is collapsing.

And every year, agents will get better, faster, cheaper, and smarter.

A chatbot answering a question is one thing.

An agent planning, executing, checking, retrying, coordinating, and finishing a task end to end is something completely different.

Human adoption of AI is massively overrated as a way to size AI demand growth.

I know this sounds stupid, wrong, and counterintuitive.

“If 2x the people use AI, won’t AI demand 2x?”

Obviously. But I think human AI adoption is mostly a lagging indicator, not a useful leading indicator.

The leading indicator that smarter investors should care about is the amount of economically valuable work that exists and can eventually be done by AI.

Human users are mostly a visible symptom of the underlying pie getting bigger.

The real driver of compute demand is not how many people open ChatGPT.

It is the total size of economically valuable work that can be automated, accelerated, or improved by AI.

So what makes compute demand go up?

1) The amount of valuable work to be done grows

2) The cost of compute goes down, because the lower the cost, the more tasks become positive ROI

3) AI becomes smarter, because that unlocks new types of work to be done by AI

Agents, not humans, are the power users of compute.

There are simply very few people who properly run the numbers and understand this.

Almost everyone is wrong. Even the smartest people in AI. And not by a little, but by orders of magnitude.

If you see this clearly, you can make life-changing returns, because the physical reality will eventually show up in demand, growth, margin expansion, and stock price performance.

I genuinely believe we are entering an age of abundance.

But the bottleneck for how quickly and how much abundance we actually get, which is funny because “bottleneck for abundance” sounds like an oxymoron, is physical infrastructure.

Digital demand can explode almost instantly because of agents.

Physical supply cannot.

That is also why I think supply constraints will most likely prevent a true bubble from forming.

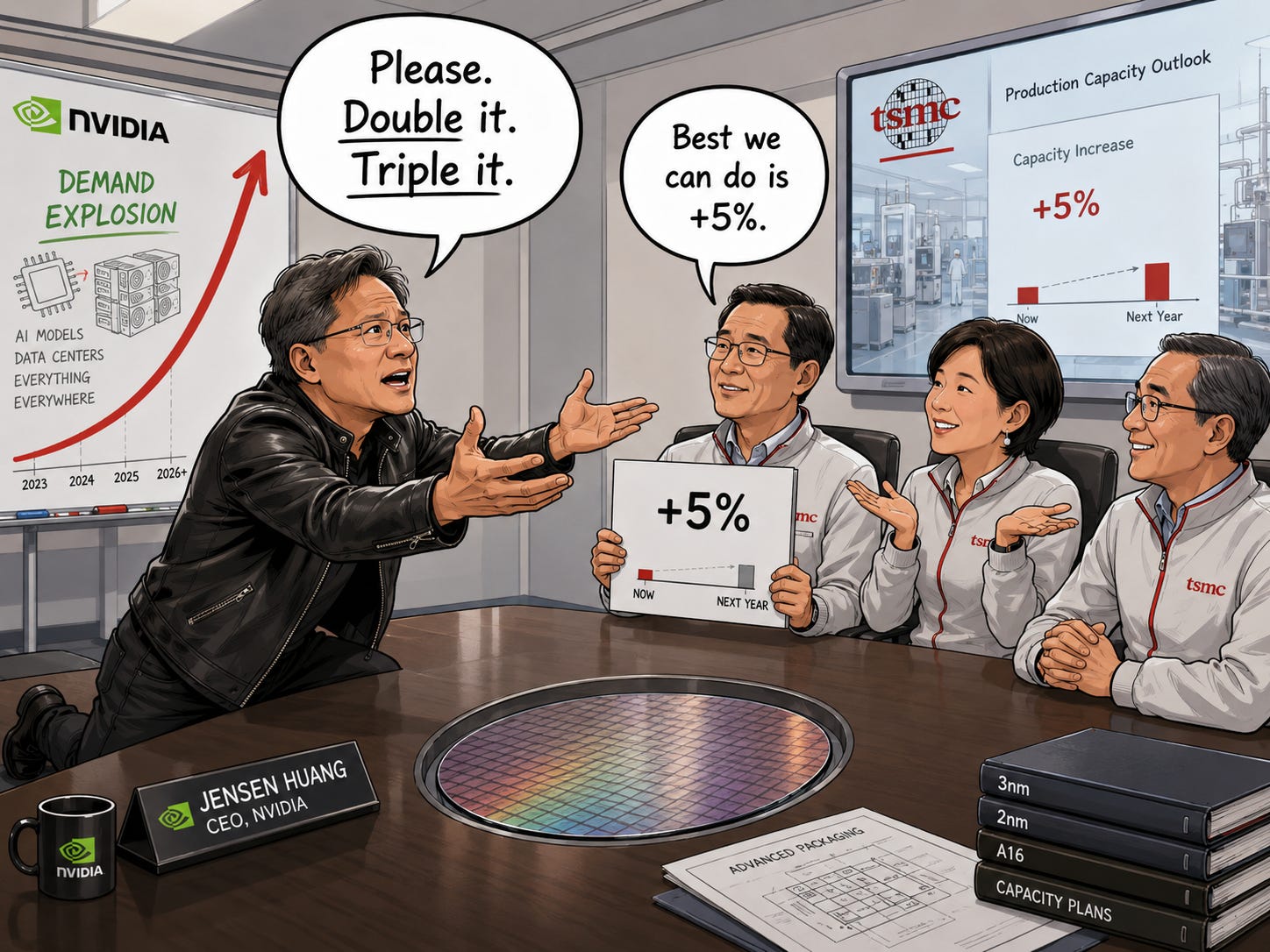

Gavin Baker made the cleanest version of this argument. His point was that bubbles (often) form when supply gets ahead of demand. But in this cycle, TSMC is not behaving like a bubble-era supplier. They are expanding slowly and rationally.

As Baker put it:

“Jensen goes to TSMC every three months, and they expand maybe 5%. Jensen wants them to double or triple capacity. If capacity actually doubled or tripled, NVIDIA could sell about $1.5 trillion worth of chips next year.”

TSMC Chairman and CEO C.C. Wei also said advanced-node capacity is still roughly three times short of AI demand.

Since TSMC is the bottleneck for almost everyone relevant in AI, supply is growing insanely slowly relative to demand.

That mismatch will be disastrously big.

This is where Nebius becomes interesting.

In a market this capacity-constrained, the winner is not simply the company that owns the most megawatts today.

A supercycle of this size will create new bottlenecks constantly.

First GPUs. Then power. Then grid access. Then cooling. Then financing. Then deployment speed. Then utilization. Then software. Then whatever bottleneck nobody is modeling yet.

So the real question is not:

“How much power do you have today?”

The real question is:

How much power can you add?

Who can build fastest?

Who can finance cheapest?

Who can deploy GPUs most efficiently?

Who can turn CapEx into ARR at the highest rate?

Who can move up the stack and increase revenue per megawatt?

Who can make the right strategic decisions again and again while the market changes underneath them?

That is why I think the main bottleneck in AI is actually the team.

The biggest long-term winner will not necessarily be the company with the biggest AI factory today.

It will be the company that becomes “the machine that creates the machines.”

And that machine is the people.

I believe Nebius has one of the best teams in the world at navigating bottlenecks, allocating capital, building infrastructure, optimizing systems, and moving up the value chain.

The team has the capacity to add more capacity, and increase the value of capacity over time.

My Quality & Risk Score

Important context: this is my own scoring system.

It is based on my research, my worldview, my investing style, and my own biases.

It is not meant to be an objective truth or a universal rating system. It is simply a way for me to compare companies consistently across the factors that matter most to me.

A score of 5/5 means excellent.

For quality factors, it means the company is elite.

For risk factors, it means I see little to no risk.

A score of 1/5 means unacceptable.

For quality factors, it means the company is weak or completely replaceable.

For risk factors, it means the risk is so high that I would usually eliminate the stock before even considering it.

Moat

I rate Nebius’ moat a 5 out of 5.

This might seem incredibly high. In the past, I initially thought the moat was a 3 out of 5. Then I bumped it up to a 4 out of 5. But today, I believe it is actually a 5 out of 5.

Here is why.

First, Nebius has extremely strong process power.

They have the highest talent density I see in any hyperscaler, and it is not even close.

They still have a startup mindset, and the ranks are stacked with very ambitious, really hardworking, intelligent, high-integrity people. I am genuinely freaking impressed by the quality of their people.

As somebody who closely monitors their hiring, I also see the quality of additional talent joining them. The talent joining often speaks a very clear language.

I see talent as a scarce resource, which is a moat. You also have to take into account that hiring the best people in this industry can take billions, so this is not a small feat.

But the culture is irreplaceable. And I think that is something you cannot buy with money.

This is the “machine that creates the machines.”

The team, the culture, the engineering depth, the execution speed, and the ability to keep solving new bottlenecks faster than competitors.

Second, Nebius has very strong cornered resources.

The most obvious one is the NVIDIA relationship.

This does not just help secure GPU access. NVIDIA invested $2 billion directly into Nebius, explicitly citing Nebius’ “unique depth of engineering expertise across the full AI technology stack.”

It gives Nebius early access to NVIDIA’s newest hardware roadmap, including Rubin, Vera CPUs, and BlueField systems. It also gives them an advantage in sales and marketing because they can ship next-generation capacity early.

It straight up gives them an unfair advantage in serving the needs of the most interesting frontier customers.

But the cornered resource is not just NVIDIA.

It is also scarce talent, hyperscaler trust, hard-to-replicate engineering culture, increasingly scarce infrastructure access, and the ability to attract serious AI customers and startups early.

None of these are fully exclusive forever. But together, they create a very hard-to-replicate resource base.

Third, Nebius has very strong scale economies.

I believe there is a compounding effect from Nebius’ day-one focus on AI, engineering efficiency, and quality.

I think this will allow them to have better margins than competitors quicker and be financially more efficient, which allows them to compound and add more capacity based on the profits from their initial capacity.

Token Factory is a good example of this.

Nebius is not just renting GPUs. They are building higher-value inference products on top. Prosus, for example, achieved up to 26x cost reductions compared to proprietary models using Nebius Token Factory.

As Nebius grows, procurement, financing, utilization, software amortization, customer acquisition, and operational efficiency should all improve.

In AI infrastructure, small efficiency advantages become enormous at scale.

So I think there is a flywheel that allows Nebius to scale more efficiently and compound faster.

Fourth, Nebius has still emerging, but ultimately very strong switching costs.

Being able to operate across the entire stack is strategically insanely valuable. It creates strong customer lock-in because Nebius can serve the same customers across multiple layers.

If Nebius only sold bare metal GPUs, switching costs would be low.

But if Nebius serves the same customer across compute, inference, optimization, orchestration, search, and eventually agentic workflows, replacing Nebius becomes much harder with every additional service the customer adopts.

This point is incredibly misunderstood by most uninformed investors in the space.

The main stickiness does not come from doing multiple things across the stack for different customers. That is just diversification of the offering.

The real stickiness and moat come from doing multiple services for the same customer.

That makes it painful to switch provider for one service, because it means the customer either has to switch between platforms or integrate different solutions.

That is painful and costs nerves, time, and money.

That simply reduces the credible alternatives customers have.

Nebius is not just best-in-class at one of those layers. To replace Nebius, you either need to find someone who can stitch together solutions across the stack, or start building stuff in-house that you probably do not want to build.

You just have very few options.

And by the way, vertical integration is something many companies in this space claim. But for most of them, it is just words in marketing. Nebius is actually vertically integrated.

Fifth, Nebius has increasingly strong branding.

Nebius has a very strong brand and very high trust in the industry because of its large-scale contracts with hyperscalers like Microsoft and Meta.

Microsoft signed a $17.4 billion five-year GPU infrastructure agreement with Nebius, with options that could expand the value to $19.4 billion.

Meta then signed a five-year agreement worth up to $27 billion, including $12 billion of dedicated capacity and up to $15 billion of additional capacity.

Nebius is becoming a trusted resource to just reliably deliver.

They are also globally diversified, currently with a strong base in the United States and Europe, and quickly expanding into APAC.

That is another very strong moat because for sovereign AI and hyperscalers, that flexibility enables not just reliability in the partner, but also creates countless options.

And for sovereign AI, you simply need local offerings.

Sixth, Nebius has emerging network effects, but I would not call them fully proven yet.

Nebius is increasingly becoming a platform for the best startups in AI.

As a result of their leading, cost-efficient offerings, they get access to the best talent early, see which companies are taking off, and can make incredibly smart and strategic acquisitions.

We have just seen this with Tavily, Eigen AI, and Clarifai.

Tavily gives Nebius the search layer for AI agents.

Eigen AI strengthens the model optimization and inference layer.

Clarifai brings system-level inference optimization, production AI expertise, and compute orchestration technology.

The more AI-native companies build on Nebius, the more Nebius can see what works, acquire strategically, improve its platform, and attract even more high-quality customers and talent.

That is the beginning of a potentially very strong and highly strategic network effect.

I have not yet seen anyone talk about that and mention how valuable this truly is to dominate long term.

The only moat source I would call weak today is counter-positioning.

It’s generally my least favorite moat, becuase it’s almost always an advantage in the beginning, but then becomes the main weapon of new challengers that take you on.

There is an argument to be made that Nebius is AI-native while legacy hyperscalers were built for general-purpose cloud and later adapted to AI.

But I would not overstate it as a crucial advantage in the long run.

It’s a focus advantage and a speed advantage and in the beginning also an efficiency advantage, but it’s not the reason why Nebius will win.

Overall, when you lay out all these components, I think the case for a 5 out of 5 moat becomes clear and strong.

Management

I rate Nebius’ management a 5 out of 5.

Insanely competent team. Strong track record. Proven execution. Reliable guidance. Clear pattern of underpromising and overdelivering.

At this point I think we all know that.

Let’s not waste time here.

Alignment

I rate Nebius’ alignment a 5 out of 5.

This is also very straightforward.

Arkady Volozh is the founder, CEO, and largest shareholder.

He owns roughly 28.7 million shares through his trust structure, plus direct equity and RSUs. At a share price of around $231, that stake is worth roughly $6.6 billion.

No matter how you look at it, the alignment is obvious and incredibly strong.

His wealth, control, reputation, and future upside are all tied to the same thing shareholders care about: Nebius becoming more valuable over time.

Execution Risk

I rate Nebius’ execution risk a 3 out of 5.

While I am biased to lower this risk because of the incredible capability of the team, this is not the section where I want that bias to influence the score too much.

As a standalone risk, execution is real.

Building AI data centers is incredibly hard. There are countless bottlenecks, shortages, and challenges across different layers: power, grid access, GPUs, cooling, financing, deployment speed, permitting, public sentiment, political pushback, competition, and more.

Even if I believe Nebius has one of the best teams in the world to navigate these challenges, the external execution risk itself is still meaningful.

The margin for error is small. Even minor construction or permitting delays can quickly turn into massive revenue misses, potentially in the billions.

If we will ever see bad earnings results from this team, this will be the reason why.

Financial Risk

I rate Nebius’ financial risk a 4 out of 5.

Nebius has a very strong balance sheet and an incredibly strong, diversified set of financing options.

They have cash on the balance sheet, strategic equity from NVIDIA, convertible debt, customer prepayments, asset-backed financing potential from large hyperscaler contracts, and operating cash flow as the business scales.

In Q1 2026 alone, Nebius raised more than $6 billion, including $2 billion from NVIDIA and roughly $4.3 billion from convertible notes.

The convertibles were also raised at attractive terms: $2.25 billion of 1.25% notes due 2031 and $1.75 billion of 2.625% notes due 2033.

The only real risk I see for shareholders is that dilution might be slightly higher than anticipated.

For that, I deduct one point.

Technology Risk

I rate Nebius’ technology risk a 5 out of 5.

The technology Nebius uses and builds is tested, proven, and works at scale.

Nebius is building AI infrastructure with technology they understand deeply and have worked with for decades.

I don’t see risk here.

Exogenous Risk

I rate Nebius’ exogenous risk a 4 out of 5.

With Nebius’ global diversification, I see very low exogenous risk.

Most exogenous factors will likely have pros and cons for them.

I am still going to deduct one point here because of potential supply chain disruptions and complications from geopolitical conflicts, trade barriers, and similar risks.

That is not a Nebius specific risk, but I only give a 5/5 score to for example defense companies who have an asymmetric relationship to geopolitical escalations where they already have massive orders confirmed and might only see those accelerate if things escalate geopolitically.